Andhra Paper Ltd

Hi fellow investor,

( Disclosure: I own shares of Andhra Paper Ltd and hence my views on the topic may be biased. Everything I conclude in the article is solely my opinion, based on publicly available information. This should not be taken as financial advice. This is purely for educational purpose.)

Let’s get straight into it.

Andhra Paper is an integrated paper and pulp manufacturer with a total production capacity of 241,000 TPA. The Company produces a range of premium grade writing, printing, copier and industrial papers for domestic and export markets. The manufacturing facilities comprise of two mills at Rajahmundry and Kadiyam, both located in the East Godavari District, in the State of Andhra Pradesh. The company was established in 1921, as “Carnatic Paper Mills”, since then the company has had multiple changes in ownership. In 2011, the Company was acquired by International Paper (IP), a $23 billion American pulp and paper company from then promoter LN Bangur. IP acquired a 75% stake in the company for around Rs 19 bn (approx. Rs 474 per share). In 2019, the controlling stake in the Company was acquired from IP by West Coast Paper Mills Ltd. West Coast acquired a 55% stake in the company from IP for Rs 6 bn (approx. Rs 274 per share) and another 17.2% through an open offer for Rs 3 bn (approx. Rs 438 per share).

The Paper Industry-

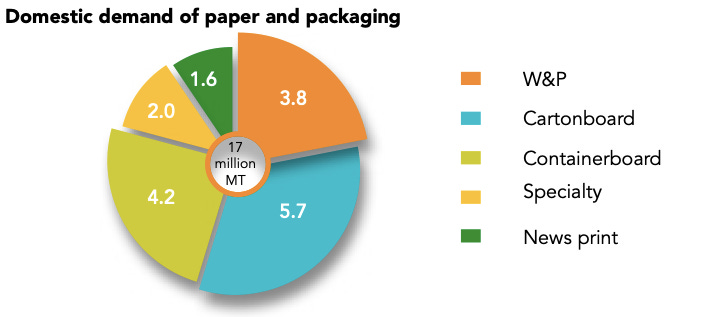

The India paper industry segmentation comprises of Writing & Printing (W&P), Cartonboard, Containerboard, Newsprint and Speciality papers. The Writing & Printing segment, in which Andhra Paper operates, accounts for ~22% of the industry capacity.

The Indian paper industry is highly fragmented with the top 3 players accounting for around 9% of the market, and small units accounting for more than 60% of the industry. Unlike countries like Indonesia & the US where the top 3 players account for more than 70% of the market, while in China it is around 21%.

Wood pulp accounts for around 30% of the raw materials used for producing paper in India. Due to limited availability of wood fibre in India, waste paper accounts for 50% and agro residue for 20% of raw materials used for paper production. The mills are dependent on imports due to the quality of raw materials.

China is the largest producer (28% share) and consumer (27% share) of paper products, followed by the US with 17-18% share in production and consumption. India accounts for 4% of the global production and 5% of the global consumption of paper products. The per capita consumption of paper in India is approx. 13kg, way behind the global average of 57kg.

The Indian paper industry added significant capacity in the first half of last decade (2011-2015), leading to over capacity. With limited supply of raw materials, it lead to pressure on raw material prices, and due to increase in supply, the producers were unable to pass on the price increases to the consumers, leading to losses for the mills.

The larger players became more cautious with their expansion plans post 2015, and looked at consolidating their position through acquisitions. In FY20, India had 861 paper mills in the country, off which only 497 were operational, showing the stress in the industry, even before Covid hit. The larger players have strengthened their balance sheets in the last five years and are in a better position to pursue inorganic expansion and secure greater economies of scale.

What lead to the improved performance for the Indian paper industry?